Back Page: The Case for Diversity

Pharmaceutical Executive

When novartis had a look at its recent M&A activity, it found something unsettling: 70 percent of the deals it had done between 1996 and 2004 hadn't delivered their expected value to shareholders. Many other Big Pharmas are saddled with the same problem: The traditional pharmaceutical business model, by which prescription drug makers scoop up assets or companies similar to their own, is going nowhere fast.

When novartis had a look at its recent M&A activity, it found something unsettling: 70 percent of the deals it had done between 1996 and 2004 hadn't delivered their expected value to shareholders. Many other Big Pharmas are saddled with the same problem: The traditional pharmaceutical business model, by which prescription drug makers scoop up assets or companies similar to their own, is going nowhere fast. Growth, so the stock market tells us (see "Trend Watch"), will be had by companies that are open to more diversified deal opportunities.

Joanna Breitstein

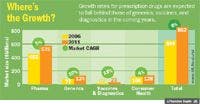

For its part, Novartis hired a hot-shot dealmaker from Deutsche Bank to reshape its M&A group. Gregory Parekh, convinced that variety adds spice and not confusion, set out to refocus corporate deals on what analysts predict will be the real growth drivers in coming years—vaccines, diagnostics, and generics (see "Where's the Growth?").

"If you look at the big M&A deals that Novartis has done," says Parekh, "they've been to build key strategic positions in areas with fast growth rates."

Consider this: Analysts expect a compound annual growth rate (CAGR) for traditional pharma companies of only five percent over the next five years. And if you subtract Plavix (clopidogrel) from the picture, that number looks more like the CAGR for consumer healthcare businesses—known to be slow earners for pharma. In contrast, industry observers expect vaccines, diagnostics, and generics to experience double-digit increases over the same period.

Trend Watch: A New Business Balance

The benefits of diversification are already being reflected in pharma companies' performances. Just track the stocks of traditional Big Pharmas against more diversified companies like Novartis—which owns significant non-pharma assets like Chiron, over-the-counter medicine Excedrin, and generics company Sandoz.

Novartis' Parekh admits that moving toward a more diversified business model is not without its challenges (see "Challenges Abound"). But then again, neither is sticking with the same strategy.

Challenges Abound Investors sometimes struggle to understand companies with multiple businesses // Core managerial competence may not be transferable across business units // Different businesses call for different employee skills sets, and different corporate cultures.

Whereôs the Growth?

Joanna Breitstein is Pharmaceutical Executive's executive editor. She can be reached at jbreitstein@advanstar.com

The Misinformation Maze: Navigating Public Health in the Digital Age

March 11th 2025Jennifer Butler, chief commercial officer of Pleio, discusses misinformation's threat to public health, where patients are turning for trustworthy health information, the industry's pivot to peer-to-patient strategies to educate patients, and more.

Navigating Distrust: Pharma in the Age of Social Media

February 18th 2025Ian Baer, Founder and CEO of Sooth, discusses how the growing distrust in social media will impact industry marketing strategies and the relationships between pharmaceutical companies and the patients they aim to serve. He also explains dark social, how to combat misinformation, closing the trust gap, and more.