- Sustainability

- DE&I

- Pandemic

- Finance

- Legal

- Technology

- Regulatory

- Global

- Pricing

- Strategy

- R&D/Clinical Trials

- Opinion

- Executive Roundtable

- Sales & Marketing

- Executive Profiles

- Leadership

- Market Access

- Patient Engagement

- Supply Chain

- Industry Trends

Pharmaceutical Product Pricing and Contracts Lifecycle Management: The Importance of Linking Strategy and Operations

Brand Insights - Thought Leadership | Paid Program

You know the saying, “You only get one chance to make a first impression”? Well, here is a similar one for pharmaceutical manufacturers: “You only get one chance to set a product’s launch price.”

Formulating an effective pricing strategy is critical to help ensure that a new product is accessible to patients and fulfills business objectives. The process is complex—the manufacturer must set both list and contract prices, being thoughtful about the long-term price trajectory inclusive of business objectives, competitive market dynamics, government pricing requirements, and price adjustments to reflect growing intrinsic value and potential indications.

Current deal constructs within the “volume/market share” archetype are relatively alike, so the contracts lifecycle management (CLM) processes and systems that companies have been using for the last 25+ years may suffice for the time being. That being said, a new environment is emerging that may upend pharmaceutical product pricing/contracting and require a new generation of CLM solutions. Among the driving forces:

- Shifting company portfolios. By 2022, >50% of both drug spending and new FDA approvals will be specialty products—often representing high per-patient costs and sizable patient impact for relatively smaller patient populations—which will require different modeling processes. What do these changes mean for pricing and contracting?

- Drugs with multiple indications. The same drug may have differential intrinsic value depending upon the indication, which creates ripple effects in the pricing process. How do you establish your list price? Do you contract by indication?

- Drug approval process acceleration. Evolving FDA standards to accelerate the standard review process for innovative and breakthrough therapies creates the opportunity for patients to receive access to new therapies with more limited clinical evidence packages. As a result, new therapies may receive regulatory approval but pose challenges to value assessment by payers. How do you consider establishing list and net pricing for breakthrough therapies with emerging clinical evidence packages?

- Introduction of cell & gene therapies (CGT) and other transformative medicines/cures. The introduction of transformative therapies, which are often curative, are frequently associated with new pricing models, causing frictions in standard payer financing and payment practices. Will these approaches require pharmaceutical companies to re-evaluate business processes and enabling applications for pricing and contracting?

- Increasing push to orchestrate and manage product pricing and contracting globally. What are the implications for global versus US pricing and contracting strategy and execution?

A company’s challenge doesn’t end once a new product’s pricing strategy is formulated and customer-specific pricing (given negotiations with the payers/pharmacy benefit managers (PBMs)/integrated delivery systems) is agreed to. Pricing and contracting strategy formulation and execution processes are intrinsically linked and should be governed/managed “end-to-end” over the life of the agreement to effectively balance patient access, affordability, and financial business objectives.

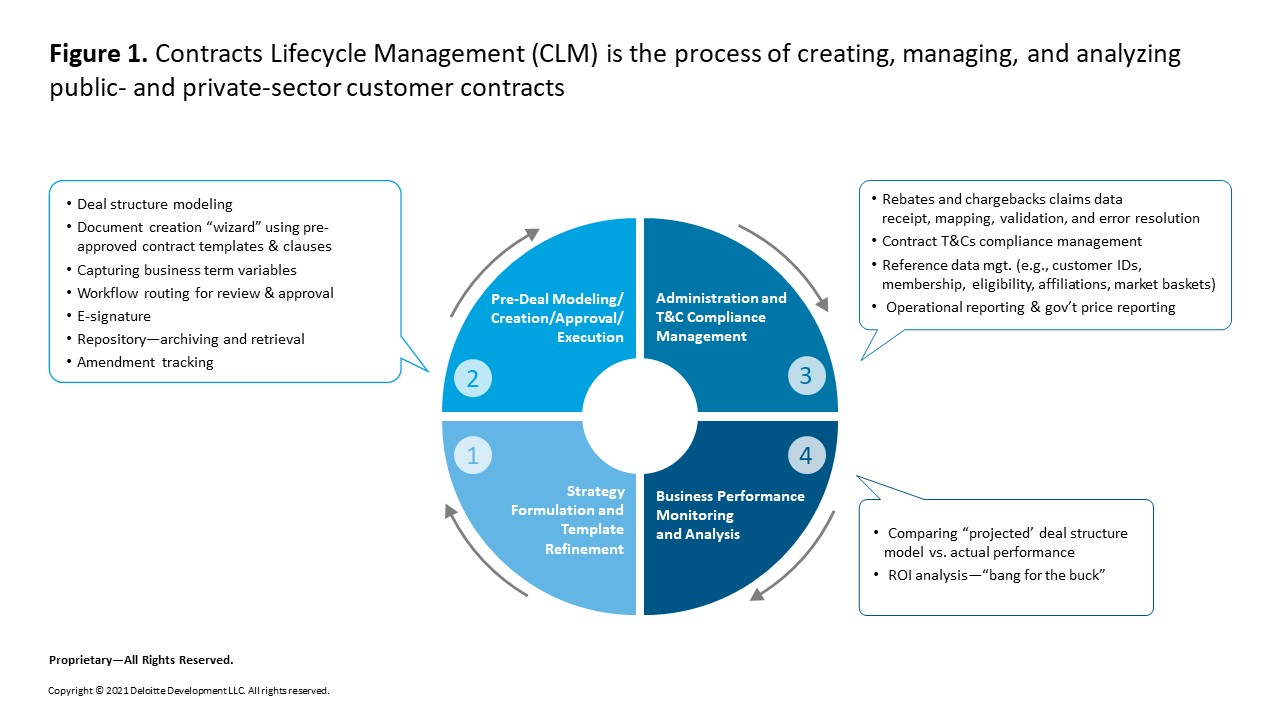

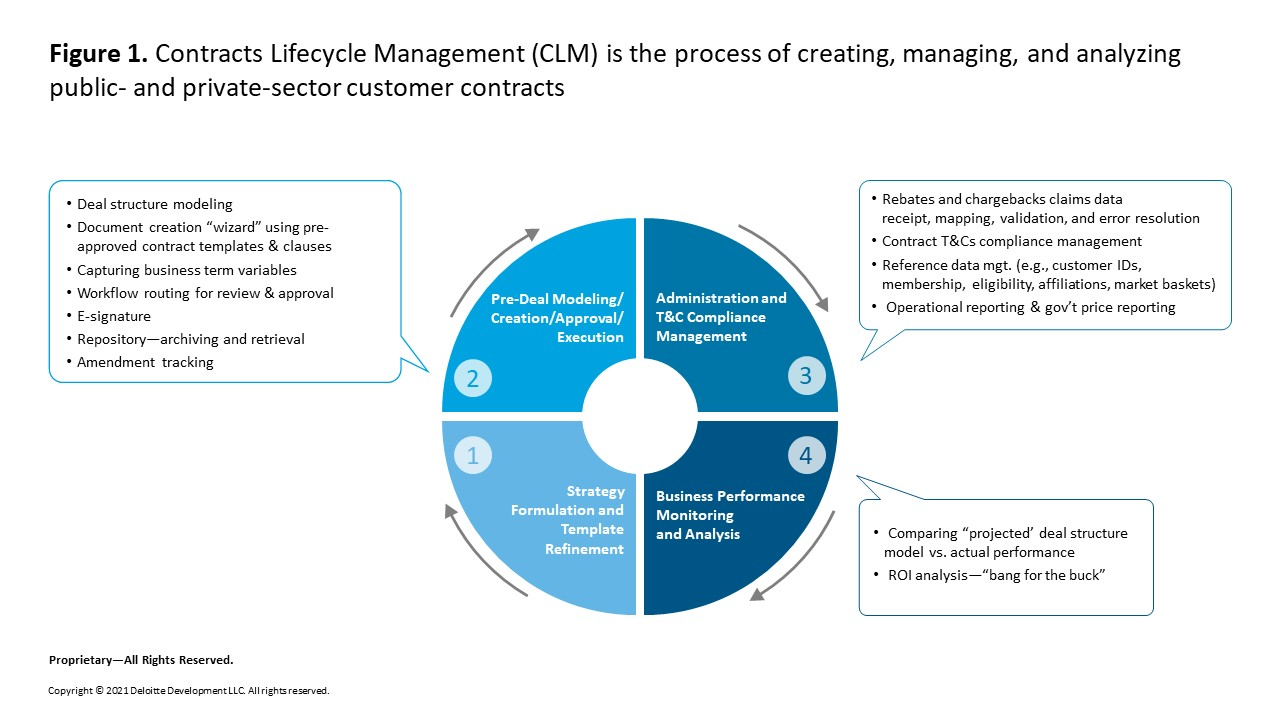

Unfortunately, within most pharmaceutical companies today, no single role/individual is ultimately accountable for the business performance of the entire pricing and contracting lifecycle (Figure 1), the process of creating, managing, and analyzing public and private sector customer contracts. Brand teams and/or payor marketing teams typically own Step 1, strategy formulation; the market access and/or finance function typically models deals and creates contracts in Step 2; and finance and/or market access manage Step 3, administration and terms and conditions (T&C) compliance management. A formal oversight role for Step 4, business performance monitoring and analysis, usually does not exist in a systematic way. As a result, this important performance data (during and after the contract’s “life”) does not routinely and systematically feed back into Step 1. In short, there is limited accountability to ensure that the pricing/contracting strategies formulated in Step 1 are performing as planned (modeled) in Step 2. The time has come to make the process, technology, and operating model changes needed to realize the business benefits of effectively orchestrating the end-to-end pricing and contracting lifecycle.

We also have often seen effective CLM stymied by the legacy systems and processes a company uses to create, manage, and analyze most contract types. These processes/systems are typically inefficient and slow, poorly controlled, non-standard, labor-intensive, not integrated, and plagued with untimely and inaccurate information. In addition, if the legacy systems and processes are not set up properly (incorporating the right affiliations, eligibility of different customer types, etc.), companies may experience financial and regulatory risks, revenue leakage, and difficulty measuring pricing/contract business performance.

Pharmaceutical companies looking to improve and modernize their legacy pricing and contract management systems should consider an integrated solution with capabilities that enable effective CLM for all types of contracts (volume-based and outcomes-based) from initial contract creation and deal modeling through ongoing T&C compliance management and contracts business performance monitoring and analysis.

Such a solution can provide tangible benefits at each of the four CLM process steps by helping companies:

- Pay the correct amount in rebates, chargebacks, and administration fees by comprehensively validating contract claims data via timely and accurate reference data (e.g., customer IDs, membership, eligibility, affiliations, formulary status, and PAR)

- Assess the near-term and long-term financial impact of private sector rebates/discounts on public sector best price (BP), average manufacturer price (AMP), average sales price (ASP), and federal supply schedule (FSS) price calculations and the respective impact on Medicaid rebate liability

- Realize optimal returns on contract-related investments by investing the “right” amount in the “right” channel customers

- Decrease the risk of paying fines and penalties associated with government regulation non-compliance (e.g., Sarbanes Oxley [SOX], Centers for Medicare & Medicaid Services, Office of Inspector General) by refining procedures/controls and implementing “smart” alerts that help ensure the completeness and accuracy of contract-related information as well as the effectiveness of underlying procedures and controls

- Confirm the government pricing system is calculating BP, AMP, Non-FAMP, FSS, FCP, and ASP correctly and according to stated business policies (e.g., class of trade) and government regulations

- Minimize rogue contracting by utilizing technology solutions that effectively control the authoring and approval processes (e.g., using a contract creation “wizard” and a repository of pre-approved alternate contract clauses and templates to automate routine legal matters for standard contracts and streamline more complex chores such as drafting and negotiating PBM and health plan agreements).

Pricing/contracting is among the top business issues that pharmaceutical company leaders face today and should be addressed throughout the entire product lifecycle, with an emphasis during launch planning and execution. A good way to begin is by answering the following questions:

- What are our short- and long-term ambitions and how can pricing and contracting levers enable us to achieve them?

- How do each of our stakeholders (payers/PBMs, patients, health care providers, policy and value assessors) experience price and what are the relevant considerations for each?

- What is the range of access barriers we are seeking to mitigate?

- What are the optimal levers (WAC price, contracting, affordability solutions) to deploy to mitigate access barriers?

- What is the mix of levers to use to achieve the total value and optimal mix, to enable us to achieve our business objectives?

- What is the timing and sequencing for which we’ll deploy these levers, through what channels, and for what duration?

- How can we operationalize the levers that we choose to apply to the prioritized customer segments?

- Do our current pricing and contracts management systems have the necessary capabilities to support a new product launch given the growing complexities of shifting product portfolios, multiple indications, new transformative medicines/cures, the shift to outcomes-based versus volume-based, and an accelerating drug approval process?

In a world where pharmaceutical manufacturers continue to seek to innovate around ways to improve patient access and demonstrate product value, advancing innovative pricing and contracting approaches is of growing importance to product launch planning and execution. Companies that designate one owner with responsibility and accountability to make the necessary process, technology, and operating model changes are more likely to realize the full business benefits of effectively orchestrating the end-to-end pricing and contracting lifecycle.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. In the United States, Deloitte refers to one or more of the US member firms of DTTL, their related entities that operate using the “Deloitte” name in the United States and their respective affiliates. Certain services may not be available to attest clients under the rules and regulations of public accounting. Please see www.deloitte.com/about to learn more about our global network of member firms. This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

Copyright © 2021 Deloitte Development LLC. All rights reserved

Value/Access/Pricing: An essential enabler for delivering on the promise of oncology innovation

The Pandemic Didn’t Hinder Drug Launches, but it Has Altered Sales Tactics