- Sustainability

- DE&I

- Pandemic

- Finance

- Legal

- Technology

- Regulatory

- Global

- Pricing

- Strategy

- R&D/Clinical Trials

- Opinion

- Executive Roundtable

- Sales & Marketing

- Executive Profiles

- Leadership

- Market Access

- Patient Engagement

- Supply Chain

- Industry Trends

Value/Access/Pricing: An essential enabler for delivering on the promise of oncology innovation

Brand Insights - Thought Leadership | Paid Program

One of the unique ties that binds all of us who work in the life sciences industry is our shared desires to make a positive impact on patients. While the industry has achieved great advances across a range of conditions, nowhere has the impact been more profound than within oncology. According to the Centers for Disease Control and Prevention (CDC), cancer death rates declined 27 percent over the past decade,1 with successes largely attributed to prevention and screening efforts and advances in treatment for a range of cancers.2 While we have achieved much progress in recent years, we have more work to do in delivering on the promise of innovations that are in development today. Successful commercialization is a critical enabler to delivering new innovations for the benefit of patients afflicted with cancer.

Oncology represents the largest and fastest growing therapeutic area (TA) within the biopharmaceutical industry, with an expected CAGR of 10 percent from 2020-20253 and global category sales anticipated to exceed $260 billion by 2025.4 In the past five years alone, 62 unique new cancer medicines have been approved in the United States, with many approved for more than one indication.5

Furthermore, most of the world’s largest life sciences companies have prioritized oncology as a critical therapeutic category for growth. In fact, the top 10 life sciences companies now account for greater than 80 percent of all oncology revenue within the United States.6 Oncology continues to command the greatest area of R&D investment, with more than 1,300 medications and vaccines currently in development.7

[1] An Update on Cancer Deaths in the United States | CDC

[2] Facts & Figures 2020 Reports Largest One-year Drop in Cancer Mortality; Annual Report to the Nation: Cancer deaths continue to drop - National Cancer Institute

[3] IQVIA Institute, June 2021.

[4] IQVIA Institute, February 2021.

[5] IQVIA Institute, May 2021.

[6] IQVIA Institute, February 2021.

[7]Report: Over 1,300 Medicines in Development for Cancer | PhRMA

The life sciences industry has delivered, and continues to deliver, transformational innovations for patients across a range of oncology conditions. Doing so requires deep understanding of the oncology ecosystem, which is complex, rapidly evolving, and associated with unique considerations relative to other specialties; among which are:

- Unique stakeholder ecosystem. The oncology health care value chain has a specialized stakeholder ecosystem, including sophisticated health care providers; guidelines and value assessment stakeholders; integrated payers, distribution, dispending, and group purchasing intermediaries; patient services; and solution providers. Life sciences companies that seek to deliver oncology innovation to patients need to effectively engage with all stakeholders in this unique ecosystem.

- Clinical and regulatory dynamism. The magnitude and pace of change within oncology is profound. Products are often approved through accelerated approval pathways or even obtain compendium support for use ahead of formal US Food and Drug Administration (FDA) approval. Furthermore, clinical comparators and standard of care within a specific indication change frequently, resulting in an environment of rapidly evolving treatment considerations.

- Criticality of value and access. Patient affordability and access enablement, along with health system sustainability and affordability, are critical factors that impact current patient access to these innovations as well as sustained future access to new innovations.

Even within oncology, there are a range of unique Value, Access, and Pricing (VAP) considerations based on product and market dynamics. These include, but are not limited to:

- Maturity of class: New class vs. established class

- Order of entry: First vs. follow-on category entrant

- Degree of competitiveness within indication or class indication

- New molecular entity (NME)/Biologic license application (BLA) launch or follow-on indication expansion

- Sequencing of indications relative to total lifecycle revenue contribution

- Role in therapy: Mono vs. combination therapy

- Line of therapy: First vs. later line

- Mode of administration (impacting access and reimbursement dynamics): Self-administration (oral) vs. health care provider (HCP) administration (e.g., infusion)

- Precision diagnostic requirements

Increasingly, launch planning and execution, whether for initial product launch or indication expansion, has become one of the most critical focus areas for oncology commercial teams. Many have dedicated business units and/or organizations with resources, capabilities, and skill sets to support successful commercialization and access. According to Deloitte research, market access has become one of the most important enablers of commercial success broadly and, increasingly, within oncology specifically.

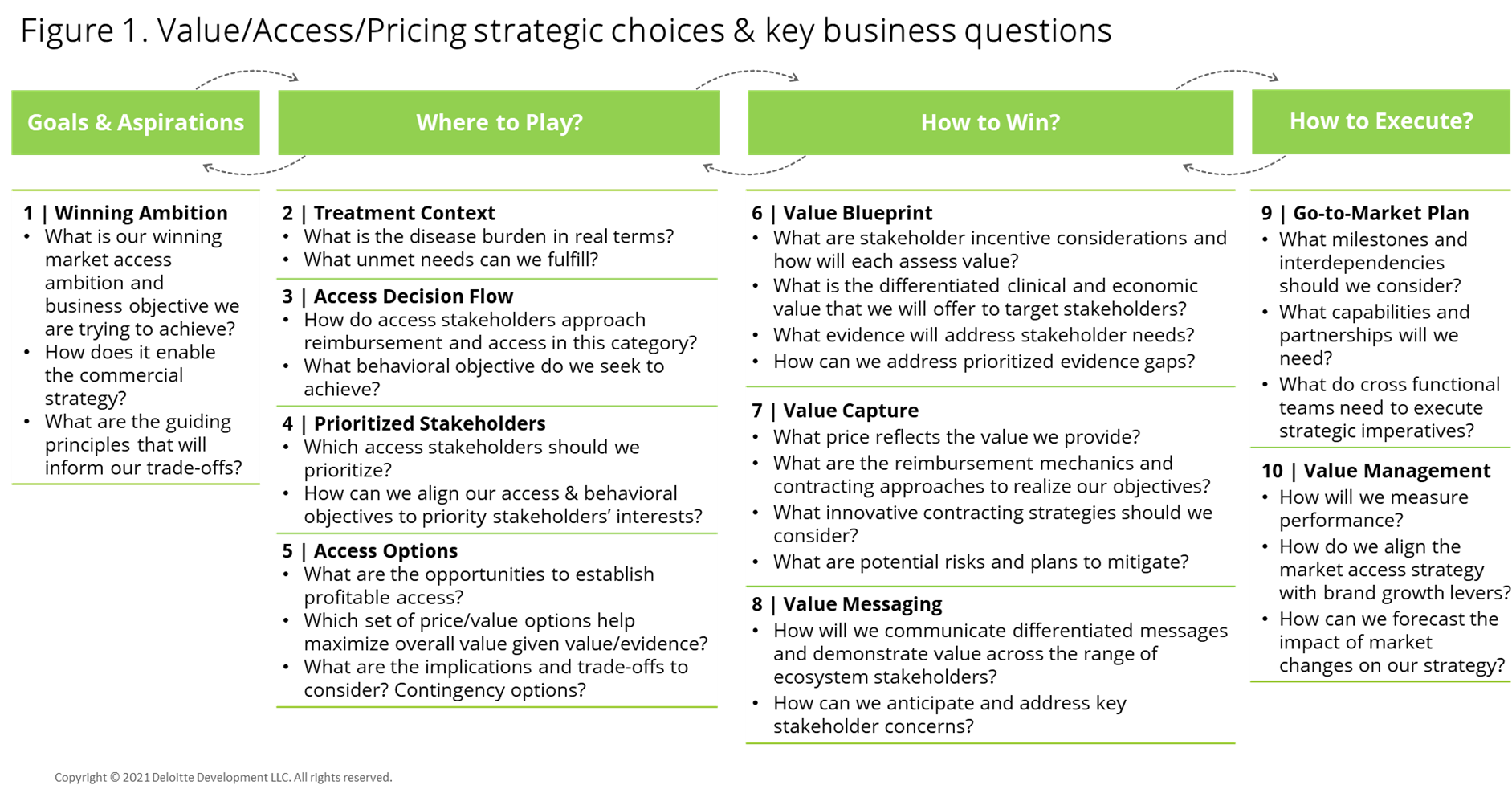

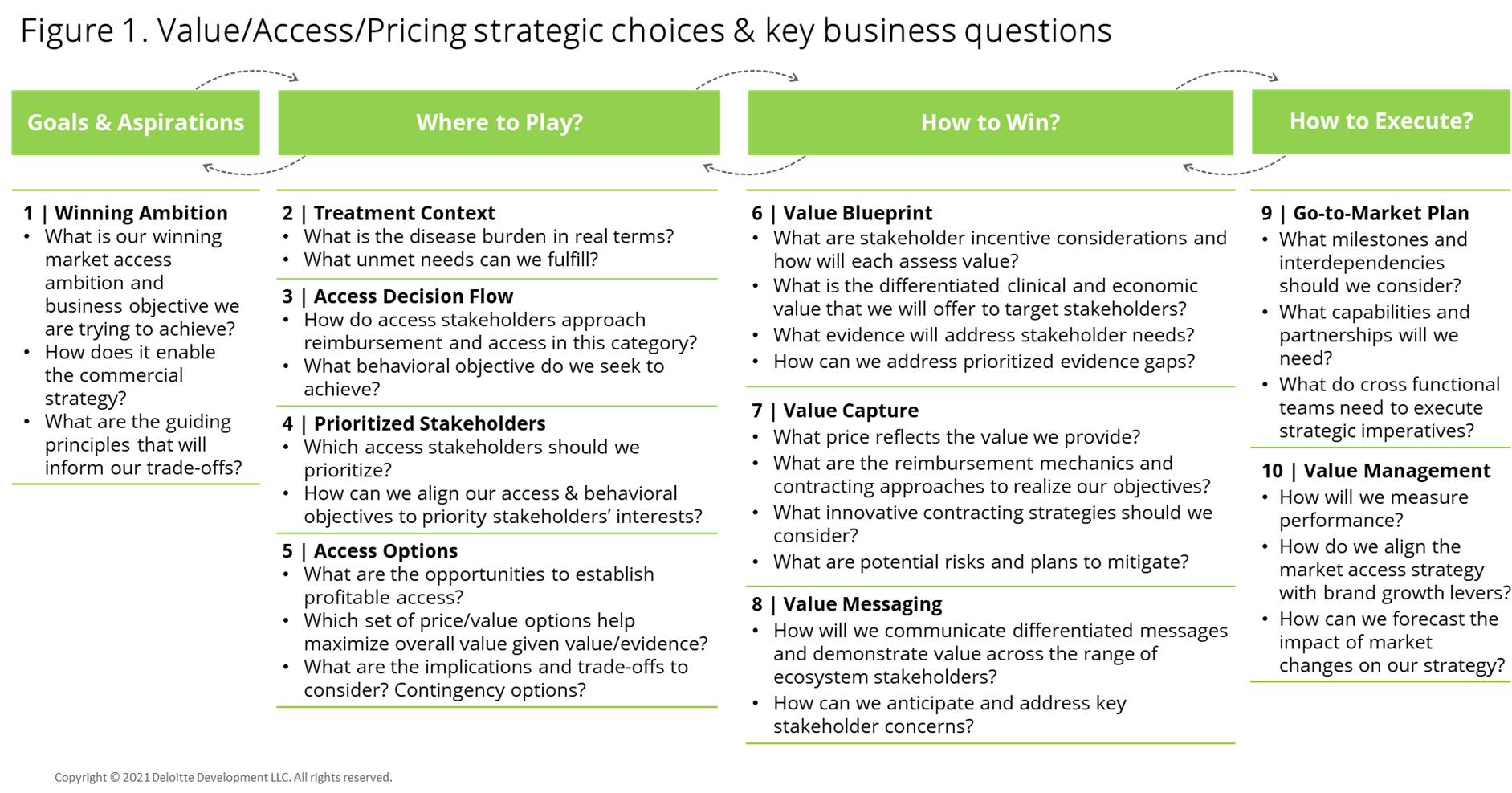

Given the evolving nature of oncology commercialization, our team has identified 10 critical “must answer” strategic questions to support and enable VAP oncology launch planning (figure 1).

In addition to the strategic choices, we have identified five common leading practices associated with successful VAP commercial launch considerations for oncology therapies:

- Initiate launch planning early (at least 24 months ahead of anticipated FDA approval), reflecting the potential for accelerated approval with pre-approval engagement and communication plan with ecosystem stakeholders.

- Align access strategy and brand strategy, including strategic imperatives and critical success factors.

- Coordinate and collaborate cross-functionally among Marketing, Value/Access/Pricing, HEOR/Evidence and Medical teams; and among payer, provider, and patient access.

- Understand oncology access ecosystem value drivers.

- Develop both launch and anticipated two-to-three-year evolution of the value/access/pricing strategy.

A company’s value, access, and pricing approach is an essential success driver for oncology-specific therapy launches. Developing defined launch plans that both accommodate the unique nature of oncology launches and align key workstreams with the VAP components can help life sciences company leaders address both the broad and nuanced considerations of an oncology therapy launch, deliver commercial success, and enable patient access to impactful oncology innovations.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. In the United States, Deloitte refers to one or more of the US member firms of DTTL, their related entities that operate using the “Deloitte” name in the United States and their respective affiliates. Certain services may not be available to attest clients under the rules and regulations of public accounting. Please see www.deloitte.com/about to learn more about our global network of member firms. This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

The Pandemic Didn’t Hinder Drug Launches, but it Has Altered Sales Tactics