China: Big Rewards. Bigger Risks?

Pharmaceutical Executive

As pharmaceutical markets go, china is a land of opportunity fraught with complex challenges. Potentially the world's largest market for prescription drugs, China is also the fastest growing market among large countries. At the same time, the sprawling system of 17,000 hospitals-the most important drug-distribution channel in China-is fragmented and encumbered by Byzantine regulations.

As pharmaceutical markets go, china is a land of opportunity fraught with complex challenges. Potentially the world's largest market for prescription drugs, China is also the fastest growing market among large countries. At the same time, the sprawling system of 17,000 hospitals—the most important drug-distribution channel in China—is fragmented and encumbered by Byzantine regulations.

Dispensing medicine keeps underfunded hospitals profitable. More than 40 percent of hospital income derives from the sale of drugs and services. In fact, 80 percent of all prescription drugs in China are dispensed through hospitals. The rest are sold by independent, retail pharmacies. Wholesalers and domestic drug manufacturers routinely supplement the low salaries of doctors and hospital executives with kickbacks and other unethical prescribing incentives. (Unlike in most Western countries, Chinese doctors are typically employees of government hospitals.)

Gu Gong, near Tiananmen Square in Beijing For hundreds of years, visitors have stood at the gates of China's Forbidden City

A complex supply chain drives up the retail price of medicine. After mark-ups by distributors and hospitals, what the consumer or provider pays can equal 20 times the price at the factory gate. Whenever government funding wanes, hospitals must find revenue elsewhere, which forces them to hike the cost of medicine further.

Large hospitals in major urban areas dominate the healthcare system, where services are concentrated in densely populated, top-tier cities like Beijing, Shanghai and Guangzhou. Although the bulk of China's population still resides in rural areas, including villages and towns, urbanization is accelerating. The old system of universal, state-subsidized healthcare has broken down and left many citizens unable to afford even the most basic treatment.

In theory, this coverage gap should be filled by health insurance—both privately funded and government subsidized—but so far the industry lags behind the demand. Cost hurdles seem insurmountable, nearly as overwhelming as the opportunity is compelling.

As diseases like severe acute respiratory syndrome (SARS) and avian flu originated in Asia and made headlines around the globe, the world health community will pressure China to address failings in the country's healthcare infrastructure.

The pharmaceutical industry is well positioned to support necessary reforms in China, leveraging its global experience to develop sound, successful cost-containment strategies. In lending this expertise, companies can hope to gain a foothold in the vast, complex, and growing market—a kind of quid pro quo. There are six key areas where pharmaceutical companies can play a significant advocacy role and help reshape the landscape of this new frontier.

1. PRIVATE INSURANCE Private insurance funded by member premiums should be developed with appropriate government support. Only three percent of the population is covered by private insurance funded by employers. Pharmaceutical companies can lead by example, providing private health insurance to employees. Moreover, they can help expand the private health insurance market by fostering relationships between local companies with key foreign and local health insurance providers.

2. AMICABLE SEPARATION Gradually, drug dispensing must be divorced from prescribing to eliminate the profit-motive, which often leads hospitals to write and dispense unnecessary prescriptions. Physicians and pharmacists must be involved in recasting the relationship between prescriber and dispenser. A pilot program should be designed to ensure an amicable separation from the outset. Economic incentives can fuel the growth of drug dispensers that operate independently of hospitals. Retail pharmacies, for instance, have begun selling drugs at a lower price than the cost charged at hospital pharmacies.

3. MARKET PRICING An independent agency established by the government should perform health technology assessments (HTA) on new drugs to ensure that actual value is created. This can help focus the industry on innovative products, and restrict me-too drugs that add no new value to the society. This is especially important as more chronic disease emerges in china as the population ages, affluence increases, and urban life becomes more prevalent.

Market pricing encourages the development of a strong, innovative industry focused on bringing new products to market that fill new needs or represent novel therapies. Conversely, significant pricing regulation risks driving the industry to a low-cost manufacturing model, which diminishes value and inhibits innovation.

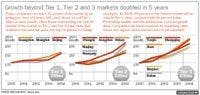

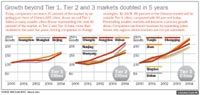

Growth beyond Tier 1. Tier 2 and 3 markets doubled in 5 years

4. IMPROVING TRANSPARENCY AND SPEED Regulatory and reimbursement processes must be overhauled to improve the transparency of new product approval and increase speed to market. The application and approval process for imported drug registration is a maze of complicated requirements, which pose serious challenges to any company seeking timely access to the Chinese market. Decision-making must be centralized—and the frequency of updates to the national reimbursement list (NRL) increased—if Chinese patients are to receive access to innovative drugs.

Pharmaceutical companies can help the government identify and execute ways to streamline and improve these processes—by using standard dossier formats from the United States and European Union, for instance.

5. IMPROVING DISEASE MANAGEMENT Adopting global clinical diagnosis and treatment guidelines, and streamlining the decision-making process surrounding disease management, help both physicians and payers. Tax breaks for the pharmaceutical industry could fund and encourage more extensive disease awareness programs in key urban areas. The pharmaceutical industry could play an important educational role, deploying sales teams to communicate guidelines and help instruct physicians.

6. PROFITING FROM PARTNERSHIP Government–industry partnerships can bring new technology and greater self-sufficiency to china, accelerating the growth of indigenous pharmaceutical companies. Moreover, a mentoring relationship can help increase employment and lower the cost of manufacturing as well as R&D.

In exchange for pricing or volume concessions on innovative products, pharmaceutical companies can transfer technology and knowledge, sharing with the government best practices in manufacturing. Companies can flex their muscles in R&D, too, by involving government labs, local innovators, and medical institutions in early-phase product development. This strategy leverages China's developing strengths in early, pre-clinical research and avoids time-sensitive research activities such as later-stage development.

No Depression

Unlocking Growth

Working with the government can spur much-needed reforms in China's healthcare environment, but pharmaceutical companies must take other actions as well to unlock growth in this market. Investing in China is one road many foreign multinational companies are choosing as they strive to create a localized infrastructure to ensure new avenues of growth and to create competitive advantage.

Case in point: AstraZeneca has made significant investments in its sales force in preparation for expansion into new city markets. More than 2,000 hospitals in 120 cities are being covered by a growing army of sales representatives, who cost the company an average of $30,000 per person per year. Investments such as these are offset by the additional revenue generated each year per rep. In larger cities, this could be as high as $200,000 per person or as low as $50,000 in smaller urban areas. The company also intends to invest $100 million in R&D in China, opening the AstraZeneca Innovation Center China in 2009. This is on top of $134 million invested in 2002 in a manufacturing plant in Wuxi and a clinical research unit in Shanghai.

Similarly, Roche has unveiled its fifth global R&D center on the outskirts of Shanghai. Novartis is collaborating with a leading Chinese R&D institute and is establishing an alliance with another Chinese biotech on other projects. In an effort to make its products more accessible to local residents, Pfizer has established a regional headquarters in Shanghai and is considering its own R&D center in China.

Investments like these become even more critical and the market opportunity more compelling as chronic disease rates rise in China with the increase of affluence. Greater prosperity often leads to lifestyle changes—for example, richer, less healthy diets—and a consequent increase in chronic diseases such as diabetes, cancer, and heart disease. By 2025, for instance, China will have 38 million diabetes patients, almost double what is projected for the United States, and about 13 percent of the global diabetic population. As China's populaton ages and people move from rural settings to more sedentary urban centers, chronic disease will grow.

Companies need to expand their efforts outside of large, tier-one cities such as Beijing, Shanghai, and Guangzhou. Today, companies can reach 80 percent of the hospital market in China by focusing on just 120 out of 665 cities. However, this dynamic is changing rapidly, so first steps must be taken toward China's future markets by understanding the shift from tier one to tiers two and three.

The real future growth will occur in cities in tiers two and three, to which rural populations are migrating. These regional centers, like Hangzhou, Shenyang, Jinan, and Tianjin, for instance, have become the key markets for highly successful drugs like Bo Le Xin, a generic version of the anti-depressant Effexor.

Improving customer base segmentation and daily call rates will also drive future growth. Segmenting by message content will also help, so that doctors who respond to efficacy or patient compliance arguments do not receive promotions based primarily on low cost. Significant growth can be driven from minimum frequency rates of one call per week on very-high-value targets and one call every two weeks on high-value targets.

Execution

All of this is easier said than done. As employers grapple with high turnover, they need to expand their talent pool into rural environs. They must invest in higher salaries, more rigorous training, and richer benefits to inspire loyalty among employees already accustomed to annual salary increases of up to 20 percent. Robust human resources programs that attract and retain top-shelf talent help companies accelerate market penetration. The companies that succeed in China will not necessarily be those with the best products. They will be companies that have marshaled the resources to execute a consistent, cohesive plan. Senior management will have to be stable. Their strategy must be informed by market-specific intelligence. And the company must be willing to forge alliances with the government.

China is the future pharmaceutical market. Companies that succeed in China will achieve higher growth rates than in mature markets around the world. Industry leaders are investing in China now. Posing the world's biggest strategic challenges, the market also promises the richest rewards.

The Misinformation Maze: Navigating Public Health in the Digital Age

March 11th 2025Jennifer Butler, chief commercial officer of Pleio, discusses misinformation's threat to public health, where patients are turning for trustworthy health information, the industry's pivot to peer-to-patient strategies to educate patients, and more.

Navigating Distrust: Pharma in the Age of Social Media

February 18th 2025Ian Baer, Founder and CEO of Sooth, discusses how the growing distrust in social media will impact industry marketing strategies and the relationships between pharmaceutical companies and the patients they aim to serve. He also explains dark social, how to combat misinformation, closing the trust gap, and more.